The Climate Intelligence Layer for Global Finance

Turn data into verified action, at enterprise scale.

Traditional Way vs. Myplan8® Way

In the traditional model, value flows from financial institutions to borrowers or consumers with little linkage to real-world climate outcomes.

Myplan8® changes this: the Green Navigator engine and Green Compass data layer embed climate intelligence across every transaction and decision point.

As a result, banks offer climate-financed products, businesses unlock verified green credit, and individuals participate in data-driven climate action.

Built for Global Scale. Measured with Precision.

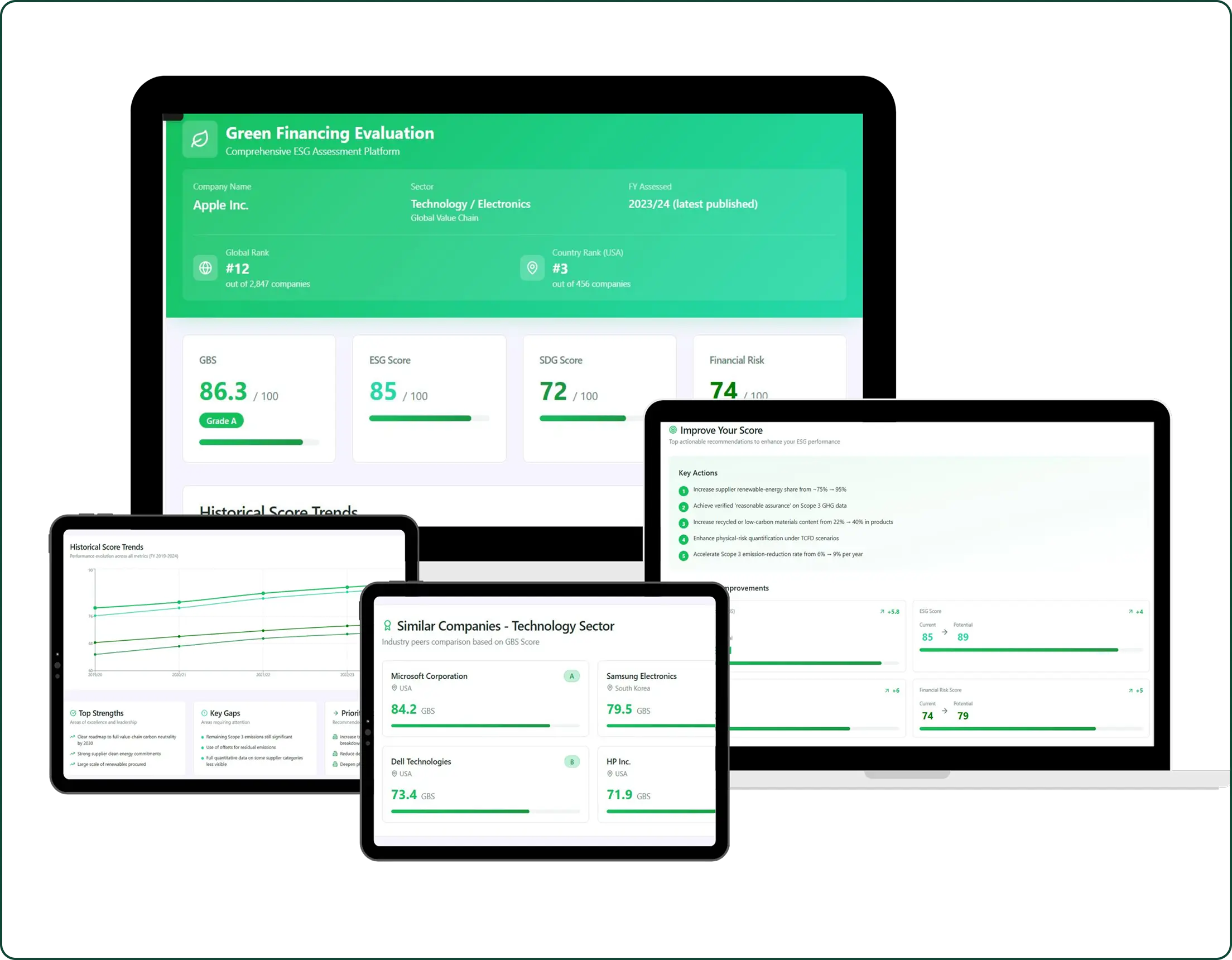

Green People Score™

measures individual behavior and lifestyle footprint against global standards.

Green Business Score™

evaluates enterprise climate performance using rigorous metrics aligned with ESG and SDG frameworks.

Green Navigator™

analyses data flows, identifies improvement pathways, and guides measurable carbon-reduction action.

Green Compass™

serves as the audit-grade data layer for ESG/SDG verification, enabling transparency and global standard reporting.

Green People Score™

measures individual behavior and lifestyle footprint against global standards.

Green Business Score™

evaluates enterprise climate performance using rigorous metrics aligned with ESG and SDG frameworks.

Green Navigator™

analyses data flows, identifies improvement pathways, and guides measurable carbon-reduction action.

Green Compass™

serves as the audit-grade data layer for ESG/SDG verification, enabling transparency and global standard reporting.

Climate Intelligence Delivered Across Ecosystems

Banks & Regulators

Integrate Myplan8® APIs to trace and optimise climate-financed flows, ESG compliance and risk modelling.

Explore Banking SolutionsBusinesses

Deploy enterprise dashboards, unlock Green Business Score™, achieve Green Place to Work® certification, and monetise verified reductions.

View Business SolutionsIndividuals

Join the data-driven journey: get your Green People Score™, earn green credits, offset your footprint and engage with climate-smart rewards.

Start Your Journey

Banks & Regulators

Integrate Myplan8® APIs to trace and optimise climate-financed flows, ESG compliance and risk modelling.

Explore Banking SolutionsBusinesses

Deploy enterprise dashboards, unlock Green Business Score™, achieve Green Place to Work® certification, and monetise verified reductions.

View Business SolutionsIndividuals

Join the data-driven journey: get your Green People Score™, earn green credits, offset your footprint and engage with climate-smart rewards.

Start Your Journey

Product that Turns Intelligence into Scalable Climate Action

Carbon iQ

A suite of intelligent APIs enabling banks and financial institutions to embed carbon analytics, ESG insights, and sustainability scoring directly into their digital ecosystems. Measure transaction-level emissions, enable green finance, and automate ESG/CBAM reporting with accuracy and scale.

Ideal For: Banks, Regulators, and Fintechs

Explore Carbon iQTransform Transactions into Verified Climate Action

Myplan8® integrates at the point of transaction — payments, supply-chains, lending, mobility, consumption — converting economic activity into measurable climate outcomes.

Every transaction becomes part of the intelligence layer, tracking, verifying and reporting impact aligned with global standards.

Leading the Change — in Numbers

With global standards baked into every data model, Myplan8® enables clients to meet international frameworks and regulatory expectations — anywhere in the world.

Tn CO₂e analysed through our platform in the past 3 years

Verified Green Workplaces & businesses

Transactions converted to climate action

Green people scores issued

Awards & Accolades

UNDP Youth CO:Lab

Winner of 2022

Green Finance Cohort

Winner of 2023 by Ahmedabad University's Venture Studio

Green Innovation of the year — Green Score™

Winner of 2024 Sustainability Awards

Powered by Verified Data, Behavioral Science & Global Standards Body

Our platform incorporates audit-grade datasets, SDG/ESG taxonomy alignment, and AI-driven analytics, delivering climate insight you can trust and scale.

We have a patent published on Green Scoring System™.

The detailed capture of all expenditures provides a rich dataset, enabling a more accurate calculation of the carbon reduction strategy.

Compliance for

Explore Carbon iQFrequently Ask Question

Turn Intelligence into Action — Globally

Whether you're a bank, business or individual, Myplan8® gives you the tools to integrate climate intelligence into your ecosystem, power real-world impact and report it globally.